e-Way Bill is an electronically generated document which is required to be created for the movement of products of more Rs. 50,000 starting with one place to another.

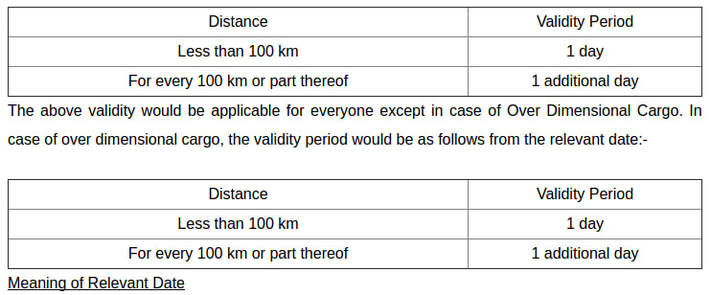

This document is required to be produced online for transportation of products regardless of whether such transportation is inter-state or intra-state. The e-way bill created in any state might be substantial in each state and association domain of India. What is the date of applicability of e-way Bill in GST? The e-way bill under GST Regime is applicale from first April 2018 for the movement of merchandise starting with one state then onto the next. For movement of product within the state, e-way bill would be presented from fifteenth April and be applicable in a staged way. The states would be partitioned into 4 parcels and e-way bill for these parts would be presented in a staged way from fifteenth April to first June 2018. The E-Way Bill under the GST Regime replaces the Way Bill which was required under the VAT Regime for the movement of Goods. The path bill under the VAT Regime was a physical archive which was required to be produced for the movement of products. The physical record under the VAT Regime has now been supplanted with an electronically created archive in the GST Regime. What is the legitimacy of an E-Way Bill? An e-way bill might be legitimate for the period as said underneath from the applicable date:- The important date with the end goal of calculation of legitimacy of the e-way bill might be the date on which the e-way bill has been produced and the time of legitimacy should be checked from the time at which the e-way bill has been created and every day should be considered the period lapsing at midnight of the day instantly following the date of age of e-way. Also Read: Know your GSTIN – What is GST Number & How to Verify? This can be clarified with the assistance of an illustration. For eg: Mr. A creates the e-path bill at 2 PM on second April. This e-way bill would be legitimate till mid-night of third April. In conditions of remarkable nature, where the merchandise can't be transported inside the legitimacy time of the e-way bill, the transporter may create another e-path bill in the wake of refreshing the points of interest in Part B of Form GST EWB 01. The Commissioner may, by warning, expand the time of legitimacy of the e-path bill for certain class of products. Who will create e-way bill?

2. In connection to a supply (Eg: Sales); or 3. For reasons other than supply (Eg: Sales Return, Branch Transfer and so forth); or

1 Comment

11/16/2022 03:08:10 am

Leave a Reply. |